All

Thought Leadership

Why hard tech exits are engineered, not found

The architecture of liquidity:

Why hard tech exits are engineered, not found

In the traditional venture capital narrative, "hard tech" is often synonymous with "patient capital", a euphemism for long horizons, capital intensity, and unpredictable liquidity. The prevailing wisdom suggests that industrial climate technologies require a decade or more to reach a meaningful exit.

At Climentum, we prefer disciplined duration. We may invest in technologies with long validation cycles when the strategic prize justifies it, but we do not confuse “hard tech” with “indefinite timelines.”

The successful acquisition of Kärnfull Next (KNXT) by Studsvik AB represents the first realized exit from our 2022 Fund I vintage 3 years after investment. Coming less than four years after the fund's inception, this transaction validates a core pillar of our strategy: In hard tech, exits are designed... not discovered. KNXT has an asset developer business model, focused on early-stage nuclear projects, before large CapEx deployments but after major value creation through stakeholder management. This capital-light approach accelerated their path to liquidity by focusing on early validation of partnerships and execution.

As we transition toward Fund II, the KNXT exit serves as a blueprint for how structure and discipline can convert industrial positioning into early DPI (Distributed to Paid-In Capital) in a sector where liquidity is notoriously scarce.

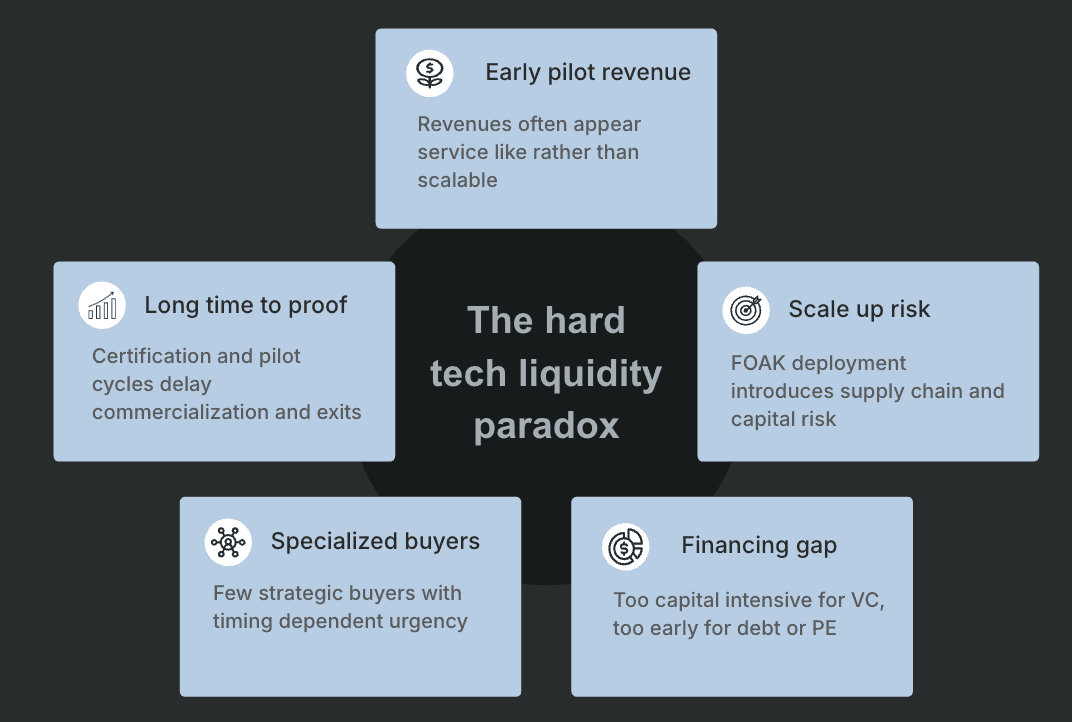

The hard tech liquidity paradox

The barriers to exiting a climate hard tech company are fundamentally different from those in the SaaS universe. While software exits typically scale on user growth and ARR multiples, hard tech exits scale on de-risked infrastructure, strategic alignment, and equity efficient planning.

Moving from technical success to a realized exit requires navigating a landscape where structural challenges frequently stall liquidity. These barriers are not just technical; they are often born from a mismatch between traditional venture habits and industrial realities.

We identify five structural challenges that typically stall hard tech liquidity:

Long time-to-proof

Hard tech requires engineering certifications, reliability testing, and long pilot cycles. This naturally extends the time-to-exit, especially if scaling proves challenging and capital intensive.

We focus on companies where the core technology is already de-risked. Our role is to provide the "scale-up" capital and strategic support, and commercial focus needed to transition from technical success to commercial dominance. Hard tech companies must prioritize focus over breadth. Instead of pursuing multiple industries, geographies, and product iterations in parallel, they need to concentrate resources on the fastest credible path to proof and commercialization.

Scale-up risk is real

Moving from a lab environment to a First-of-a-Kind (FOAK) plant introduces supply chain fragility and unit economic volatility that pure software investors are rarely equipped to underwrite.

We prioritize capital-light manufacturing models and robust supply chain design to ensure scaling doesn't erode the company's valuation. From the beginning, we screen for ventures with clear scaling potential on all key vectors.

Buyers are often specialized

Hard tech buyers are often specialized OEMs or industrial strategics driven by rigid internal roadmaps. Strategic fit is a prerequisite, but it isn't enough; the buyer must also have the capacity and urgency to act.

We pressure-test tangible urgency at the point of investment. We don't just ask "who buys this?" but "why must they buy this now?" We also map a broader set of buyers across multiple geographies to avoid being hostage to a single strategic roadmap.

Revenue can look ‘non-venture’-like

Early-stage hard tech revenue often looks like "engineering services" or bespoke pilots. Traditional VCs often penalize this as non-scalable.

We view these early pilots as critical validation. However, we work relentlessly with founders to transition these into repeatable product revenue and prioritized recurring service models that command higher multiples.

The financing Valley of Death

Many hard tech companies enter a structural financing gap. They are too capital intensive for traditional venture follow on rounds, yet not sufficiently cash flow stable for Private Equity or conventional debt. As a result, they often depend on generalist investors who lack the specialized expertise required for physical scaling across financial, operational, and commercial dimensions.

We address this gap through deliberate underwriting and portfolio construction. From entry, we design the full fundraising pathway rather than financing round by round. Our portfolios are structured to accommodate bridge rounds where needed, and to anticipate capital intensity rather than react to it.

Our specialization enables active support in financial scaling. This includes structuring larger and more complex rounds such as hybrid debt and equity for first of a kind assets, designing asset light expansion strategies, and securing national and regional grant funding.

The objective is equity efficiency. We combine milestone based value creation with hybrid and non dilutive capital to reach scale without eroding founder ownership or weakening exit leverage.

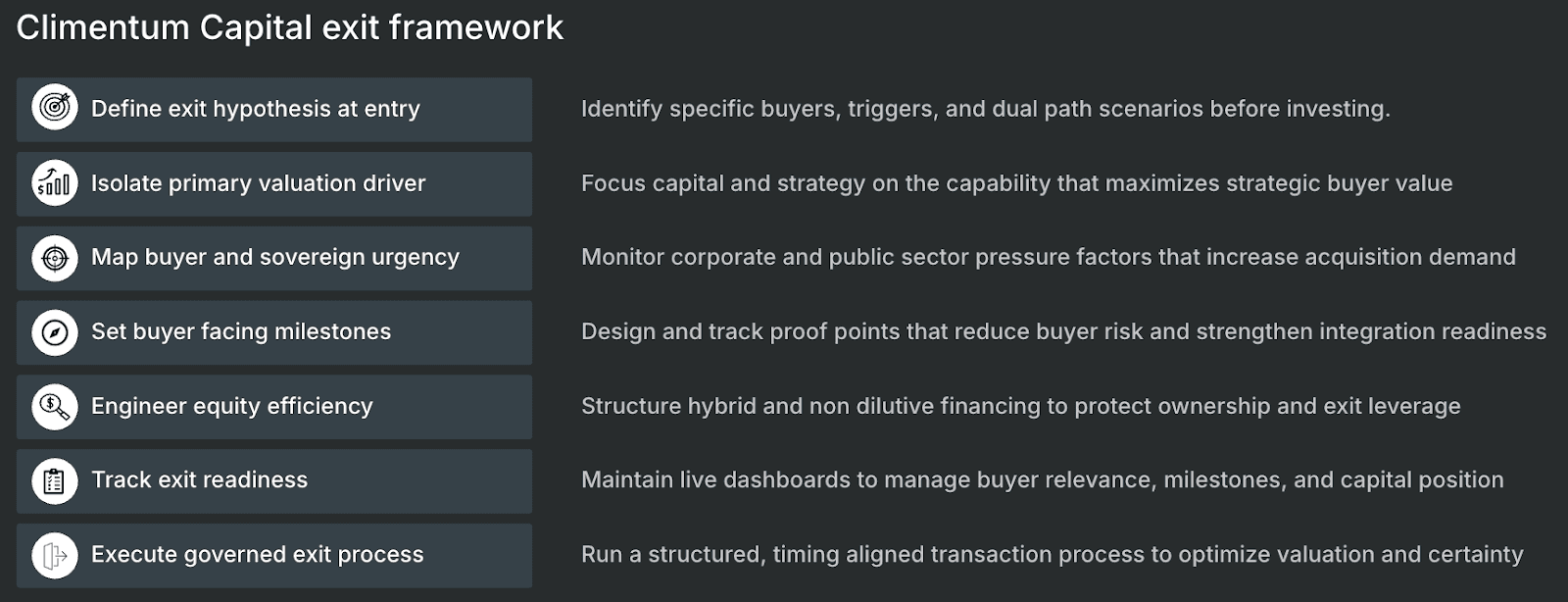

The Climentum exit framework: Discipline of readiness

We approach exit strategy as both a structured discipline and a continuous mindset from diligence through realization. The KNXT exit was the direct result of applying this seven-step framework:

1. Defining the exit hypothesis at entry

We do not invest on a "hope and a prayer" that a buyer will emerge. We pressure-test the exit route before the term sheet is signed: Who specifically buys this? Why now? What is the trigger? We define a "Fastest Credible Path" versus a "Value Maximization Path" and pivot based on market signals.

2. Identifying the primary valuation driver

Buyers rarely value everything equally. For KNXT, the value wasn't in heavy reactor manufacturing, but in its role as a capital-light orchestrator, a developer model that handled the complex permitting, siting, and commercial structuring of nuclear new-builds. We focused the company’s resources on perfecting this "orchestrator" role, making them an irresistible bolt-on for an established player like Studsvik.

3. Mapping buyer urgency

Strategic fit is useless without urgency. We monitor the "Buyer Readiness" of the top 10 potential acquirers in every portfolio company’s sector. We look for external pressures (decarbonization mandates, energy security crises, or competitor moves) that turn a "nice-to-have" technology into a "must-acquire" asset. In selected sectors, we also consider public sector demand as a potential exit pathway. As Europe strengthens its focus on industrial resilience and sovereignty, governments and state affiliated entities may become relevant counterparties, either directly through strategic acquisitions or indirectly through national consolidation efforts.

4. Defining and tracking buyer-facing milestones

Together with the startup, we specify commercial, financial, and operational milestones specifically designed to reduce buyer risk. Each marker is chosen to increase a strategic’s willingness to pay by proving reliability and integration readiness long before the formal M&A process begins.

5. Engineering equity efficiency

One of the greatest threats to a successful exit is unnecessary dilution. By combining equity with non-dilutive grants and asset-backed structures, we ensure the cap table remains "exit-friendly." This preserved our negotiating leverage during the Studsvik negotiations.

6. Systematic progress tracking

Exit readiness is monitored continuously, not episodically. We use professional tools to maintain exit dashboards for each portfolio company. By regularly updating buyer relevance, milestone completion, and capital position, we ensure the board always has maximum optionality. This assessment is reviewed across the full Climentum team to leverage our network and broader ecosystem, ensuring strategic relevance and coordinated support across geographies.

7. Running a governed exit process

A successful transaction is the result of years of positioning, but the final execution requires its own discipline. We typically begin a governed exit process 18–24 months before the target completion date. This runway allows us to align the company’s final performance peaks with the buyer’s internal planning cycles, ensuring a seamless transition and maximized value.

Contextualizing success: The DPI reality

To understand why a 2026 exit from an investment from 2023 in a 2022 vintage fund is significant, one must look at the broader venture landscape. In the last decade, venture funds have focused on book value increases, not on DPI. According to industry benchmarks, the median DPI for a VC fund at year eight is approximately 0.27x, with many funds not reaching 1.0x (returning the initial capital) until year 12 or 15 (PitchBook).

The traditional IPO pathway remains narrow. Only 19 VC-backed IPOs occurred in Europe in 2025 — a record low . Moreover, nearly 90% of IPOs are now profitable at listing, raising the bar materially for venture-backed companies. Instead, liquidity has migrated toward other channels. Acquisitions represented 46.4% of total exit value in 2025, while buyouts increased their share to 28.1%. In parallel, secondary markets are institutionalizing. European liquidity is increasingly architected across strategic M&A, private equity, and structured secondaries.

For a deep tech fund to produce a realized exit in its fourth year is a clear signal of process over luck. It demonstrates that the European industrial transition is creating a "liquidity reset", where strategic buyers are now willing to pay for credible, de-risked climate solutions long before they reach IPO scale. This is foundational for Climentum's exit strategy, pursuing meaningful and timely DPI for investors.

Looking ahead: The pipeline of "engineered exits"

KNXT is the first proof point, but it is not an outlier. Our portfolio currently contains several "exit-ready" industrial platforms moving through defined milestones:

Qvantum (Sweden): As they scale their modular heat pump manufacturing, we are moving beyond venture milestones toward IPO readiness. This involves professionalizing governance and stabilizing recurring service revenues to meet public market underwriting standards.

Enerin (Norway): They are currently deepening a strategic partnership with a key customer and potential acquirer, Johnson Controls (JCI). This is a classic example of our "Buyer-Facing Milestone" strategy, demonstrating reliability within a buyer’s own ecosystem to reduce the friction of an eventual acquisition.

Conclusion

The "long game" of climate tech does not have to be a "slow game." By applying a disciplined, engineered approach to liquidity, we are proving that hard tech can deliver the returns and the DPI that institutional investors demand.

The acquisition of KNXT is a milestone for Climentum, but more importantly, it is a signal to the market: Europe’s industrial transformation is underway, and the pathways to liquidity are open for those with the discipline to design them.